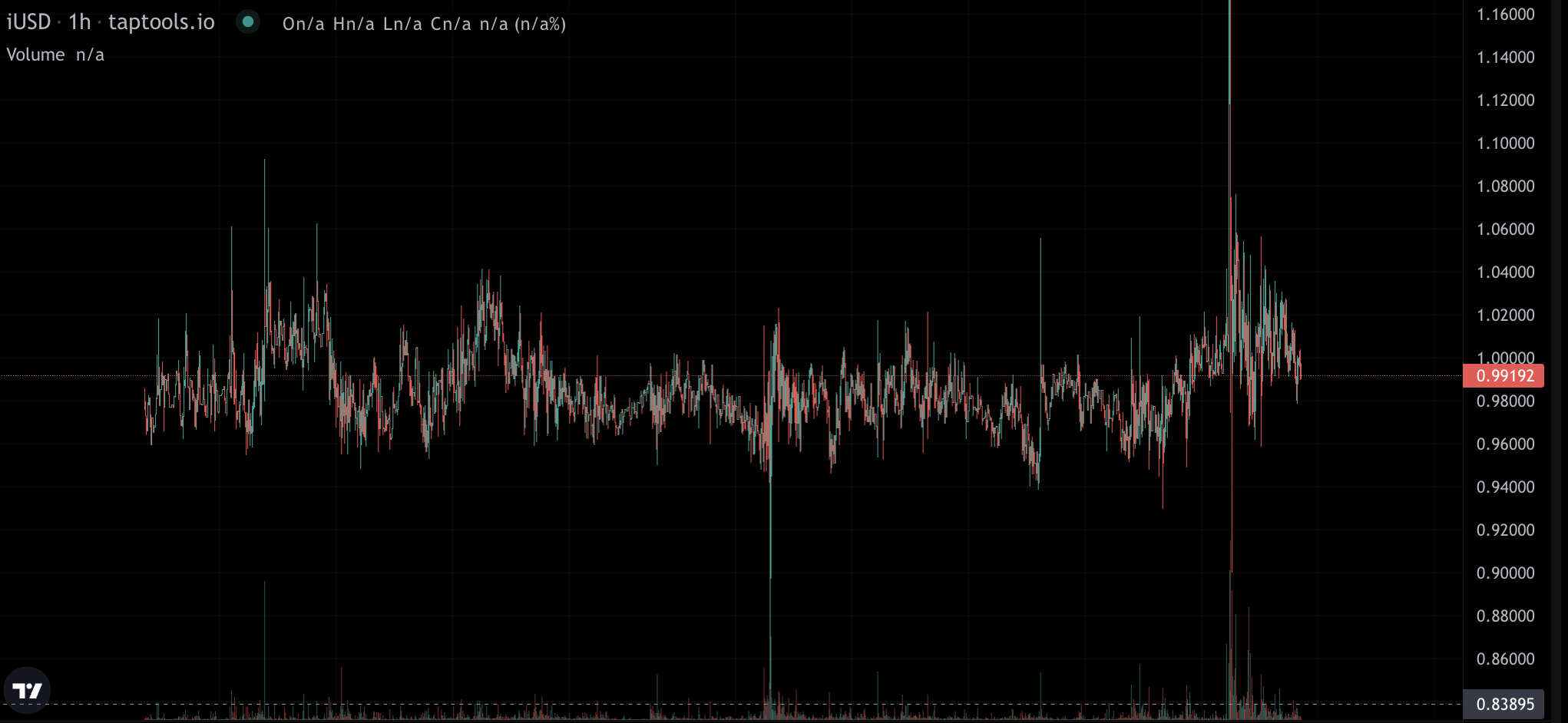

So we have seen that with the current parameters, our iAssets peg have been holding quite well compared to before. That being said, the protocol still tolerates significant enough depeg to occur for, in my opinion, an extended period of time.

Even if we do, we don’t exactly have a way to prioritize which CDP to redeem against first

Since the protocol tolerates depegs, spot users doesn’t treat iAssets as the synthetic version of the asset, so they don’t use them as such. (They don’t buy them when they depeg since there’s no confidence it’ll regain peg within a fixed amount of timeframe)

Here’s what I propose we do:

Make redemption centralized controlled by either the foundation or the labs. Most, if not all, profits should go to the DAO.

Implement unlimited redemption

Design a prioritization for which CDP/CDPs should get redeemed first

DAO-controlled formula that controls when redemption should start to occur. My idea right now is, X amount of days where iAsset market price is below Peg-Y%

Since this would practically make RMR parameter, a new formula for variable interest rate would need to be made.

Heavily cut maximum interest to at least under 20%. This is arbitrary, maybe you guys can come up with a better number, but it needs to go down heavily.

The obvious negative of this would be that it’s centralized but I think it’s worth it if we can give users confidence that iAsset will have a super strong peg.

That’s all for now, I’ll update this post according to how this discussion goes. Let me know what you guys think.

Hello,

Just my 2 cents: assuming that the free market undervalues an iAsset for “too long”, the protocol would end up with a huge amount of an iAsset that is no longer worth enough.

We’d have to think about a threshold beyond which this no longer happens… or something like that, I don’t know.

It’s hard for me to accept this idea as it is.

Sorry, I’d misunderstood your initial point: I thought that the protocol itself would end up accumulating too many devalued iAssets, which could pose a problem. But if the idea is precisely to burn the iAsset, then it makes more sense.

There is few points I’m still curious about, though: how can we ensure that this buy-back & auto redemption mechanism doesn’t create other imbalances, for example by favouring certain CDPs over others ?

What exact parameters should be used to decide when a buyback is necessary ? Is it based solely on the market price, or should other indicators such as market depth or recent volatility also be taken into account ?

Just brainstroming.

There is few points I’m still curious about, though: how can we ensure that this buy-back & auto redemption mechanism doesn’t create other imbalances, for example by favouring certain CDPs over others ?

This is why I’m still not sure about the criteria of which CDP to redeem first. We can do things like

The lowest Collateral Ratio

The one that hasn’t paid interest the longest

Perhaps we can redeem N amount of CDP with the lowest CR/ hasn’t paid interest the longest at once so that they don’t get redeemed as much

What exact parameters should be used to decide when a buyback is necessary? Is it based solely on the market price, or should other indicators such as market depth or recent volatility also be taken into account ?

My current idea right now would introduce 2 parameters,

Depeg Time Tolerance (DTT) amount of time the protocol will tolerate depeg

Depeg Price Tolerance (DPT) is the standard deviation the system will tolerate (won’t redeem)

So the system will only start to redeem once it detects that iAsset A has been priced under 100-DPT% for more than DTT amount of time.

does that mean you also don’t see much use of the current redemption mechanism? if so then I guess, we just straight up disagree. only CDP users can realize the value of iAsset without redemption.